As cleantech investors in gaseous energy including natural gas, hydrogen gas and renewable natural gas, NGIF Capital closely follows government policy as it relates to energy technologies. When the Inflation Reduction Act (IRA) was signed into law on August 16, 2022 it sent shockwaves across the cleantech landscape. The IRA contemplates enormous financial incentives to rapidly accelerate the commercialization of clean energy technologies. The IRA’s federal clean growth incentives are estimated to be USD$369 billion, though a number of observers estimate the IRA could mobilize as much as USD$1.7 trillion over the next ten years. The impact of the IRA was so pronounced that the Canadian government made its’ response a centerpiece in the 2022 Fall Economic Statement (FES) the following November. To maintain Canadian competitiveness, the federal government outlined its plan to implement three clean technology tax credits:

Each of these schemes offers companies a refundable credit of up to 60%, 30%, and 40% of capital costs, respectively, subject to various factors that modify those amounts. On March 28th, 2023 the 2023 Federal Budget was released and while major elements of both the CCUS and Clean Technologies tax credits are still under development, Canada’s budget announcement provided rich details on the Clean Hydrogen tax credit. In part one of this insight series, we are going to explore a direct comparison between the hydrogen subsidies from across the 49th parallel and what they mean for participants along the natural gas value chain.

Both Canada and the United States have identified the need to supplement commercial-scale hydrogen production as the cornerstones of their respective emission reduction strategies. The primary objectives of both countries are to exponentially grow domestic hydrogen production while simultaneously incentivizing the move away from grey hydrogen (produced from natural gas without CCUS) and towards a technicolour rainbow of blue, green, yellow, and turquoise production methods. However, despite their common objectives, each country is relying on different mechanisms to incentive investment into low-carbon hydrogen production.

Canada’s Clean Hydrogen Investment Tax Credit (ITC) provides direct subsidies for capital costs associated with the purchase of equipment to produce ‘clean hydrogen’, as determined by a project’s carbon intensity (CI) (kg CO2e/kg H2 produced). The ITC provides subsidies for the purchase and installation of hydrogen production equipment between March 27, 2023 and December 31, 2034, after which the Hydrogen ITC will be phased out. The levels of support vary between 15% – 40% of eligible project costs, assuming all labour requirements are met. Projects that produce the cleanest hydrogen will receive the highest levels of support. Critically for the natural gas industry, “equipment required to produce hydrogen from natural gas with emissions abated using CCUS would be eligible for the Hydrogen ITC.”

|

Canada’s Clean Hydrogen Investment Tax Credit

|

| Carbon Intensity Tiers (kg CO2e/kg H2) |

Tax Credit Rate (applied to eligible costs) |

| <0.75 |

40% |

| 0.57 – 2.0 |

25% |

| 2.0 – 4.0 kg |

15% |

| >4 kg |

N.A. |

Meanwhile the IRA offers hydrogen producers a choice between two mutually exclusive credits aimed at reducing the burden of either capex or opex for new hydrogen projects. Like Canada’s Hydrogen scheme, the IRA segments projects into tiers, with the lowest CI hydrogen receiving the largest levels of support. The IRA designates a hydrogen project as ‘clean’ if they produce <4 kg CO2e/kg H2 (measured on a lifecycle basis). For comparison purposes, carbon emissions associated with grey hydrogen range from 10 – 12kg CO2e/kg H2. Under Section 48 of the IRA, clean hydrogen project proponents can claim an Investment Tax Credit for clean hydrogen projects for support of up to 30% of total eligible project costs depending on its emissions intensity, and wage and apprenticeship requirements.

|

IRA’s Hydrogen Investment Tax Credit

|

|

Carbon Intensity Tiers (kg CO2e/kg H2)

|

Portion of project costs claimable as credit |

Tax credit with wage and apprenticeship conditions

|

|

0 – 0.45

|

6% |

30% of project costs

|

|

0.45 – 1.5

|

2% |

10% of project costs

|

|

1.5 – 2.5

|

1.5% |

7.5% of project costs

|

| 2.5 – 4.0 |

1.2%

|

6% of project costs

|

Alternatively, under Section 45V of the IRA, producers of clean hydrogen can qualify for a Production Tax Credit, which makes payments over a 10-year period. These production tax credits can range from USD$3.0/kg for hydrogen produced with a CI < 0.5, to USD$0.60/kg for hydrogen produced with a CI between 2.5 and 4.0. Hydrogen producers must choose between the two credits. Only one of the Production or Investment Tax Credit can be applied to a single hydrogen project based in the United States.

|

IRA’s Hydrogen Production Tax Credit

|

|

Carbon Intensity Tiers (kg CO2e/kg H2)

|

Tax Credit (USD$/kg H2)

|

|

0 – 0.45

|

$3.00

|

|

0.45 – 1.5

|

$1.02

|

|

1.5 – 2.5

|

$0.75

|

|

2.5 – 4.0

|

$0.60

|

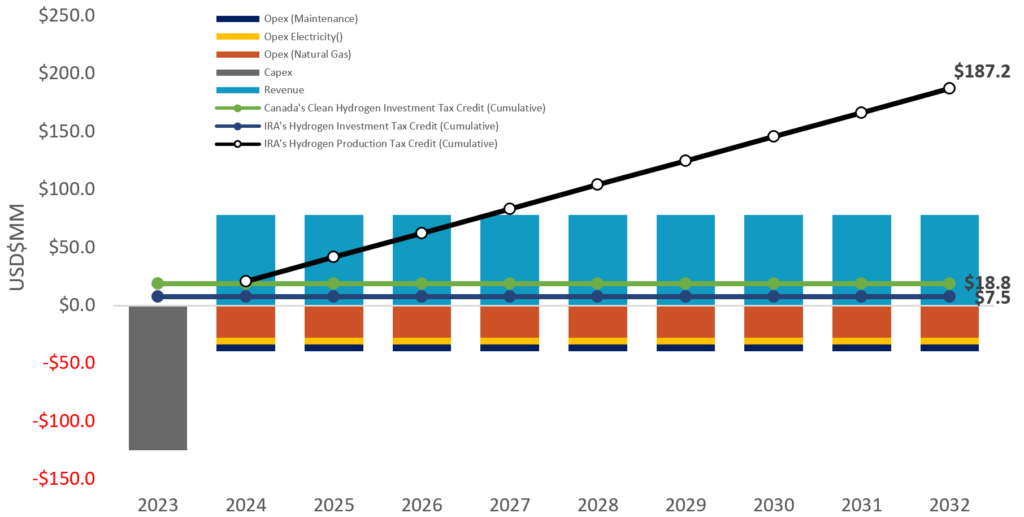

Each subsidy will help to catalyze the commercialization of large-scale hydrogen production in both Canada and the United States. However, the magnitude of financial support from the IRA creates a compelling financial incentive for the commercial deployment of hydrogen production facilities in the United States. Take for example a hypothetical USD$125MM 100 TPD blue hydrogen production facility that utilizes Steam Methane Reforming with CCUS. This project utilizes 1 GJ of natural gas to produce 3.8 kg H2 and 14 kg C for a carbon intensity of 3.7 (14 kg C/3.8 kg H2). Depending on location, and assuming all labour requirements are met, this project would qualify for one of the following subsidies:

- 15% Investment Tax Credit (Canada)

- 6% Investment Tax Credit (IRA)

- USD$0.60/kg H2 Production Tax Credit (IRA)

On an investment basis, the Canadian subsides provide a greater financial incentive (15% vs 6% of eligible capex) to construct the project in Canada. The subsides provide approximately USD$18.8MM in tax credits for a project located in Canada versus USD$7.5MM for one in the United States. However, the IRA’s Production Tax Credit would offer that same producer USD$187.2MM (USD$0.60/kg H2 x 100 TPD x 10 years) over a ten-year period for a project located in the United States – nearly ten times the financial incentive currently being offered in Canada. This analysis highlights a clear shortcoming in the current Canadian incentive scheme, and one that will need to be rectified quickly to maintain the country’s competitiveness in the rapidly evolving hydrogen economy.

Assumes 100 TPD facility operating at 95% capacity for 365 days/year. Hydrogen is sold for USD$2.25/kg. Natural gas is consumed at a rate of 266 Gj/Tonne H2, at a cost of USD$3.00/Gj. Electricity is consumed at 0.10 MW/Tonne H2 at a cost of USD$70.00/MWh. Maintenance is assumed to be 5% of the USD$125MM capex per year.

It is clear that both regimes are attempting to transition away from grey hydrogen in favour of alternative commercial-scale low-carbon methods. However, while the U.S. is using the ‘carrot’ approach with enticing subsidies to incentivize the shift, Canada has elected to use the ‘stick’. “Canada has one of the most ambitious carbon pricing programs in the world”, which penalizes grey hydrogen producers, increases the associated production cost, and reduces the relative attractiveness of that option. This stands in sharp contrast to the U.S., which does not have a carbon price at the federal level (although some states in the union have enacted carbon pricing at the local level). Therefore, Canada is banking on the effects of its carbon price, which effectively reduces the size and scope of the necessary tax credits required to effectively incentivize the desired action. In practice, this methodology effectively disincentivizes the production of grey hydrogen, but a lack of meaningful subsidies fails to properly compensate producers of lower carbon alternatives.

Furthermore, production tax credits are largely viewed by economists as a more efficient mechanism compared to investment tax credits. This is because production incentives are more closely aligned to the final policy objectives – which in this case is the production of clean hydrogen. It has been argued that investment tax credits are less effective because not all projects successfully reach maturity, and project costs are not uniform when controlled for the same outcome. Therefore, in order to compete more closely with the U.S. it will be critical for Canada to expand the recently announced Hydrogen ITC to include production based milestones for the amount of actual clean hydrogen produced. While it is encouraging to see the Canadian government’s commitment to hydrogen development, it is clear that more work is needed to maintain our competitiveness as a key player in the hydrogen economy. Canadian entrepreneurs are some of the best in the world, and NGIF Capital is committed to investing through its Cleantech Ventures fund in those pioneers who are developing the next generation of truly disruptive gaseous energy technologies.